Investments

Investments are a critical tool to ensure one’s financial future. This is an area that if you follow the lessons in this book, this will likely be the largest source of your income over your lifetime. In the first part of your career, your earnings will be mostly derived from employment income, then it will move to business income or perhaps rental income but over time, this should be your number one source of income.

If you follow the basic steps and lessons outlined in this book, you will have employment income, you will learn how to budget and save a significant portion of that employment income. In this chapter we will show you how to invest those savings, then not too far into the future, there will be a time where your investment income earns more per year than your salary, this will continue and if you start early enough, it is possible that your investment income is about ten times your employment income. We have shown examples where a person earning $50,000 per year can save and ultimately earn about $500,000 per year in investment income. Of course, we would advise retiring before this, with the one caveat that you truly love your job and would do it for free, in that case, it would be good to continue with your employment, otherwise, it would be time to enjoy your life as you like and retire.

What type of instruments do we advocate to use and which methodology? We do not advocate day trading, we advocate the polar opposite to day trading. The best and most successful strategy is to buy and hold for the long run. Only sell when you must. This is a critical concept. Whatever investments you purchase are to be held for the rest of your life or at least until retirement age. When you decide to retire, it is critical that you have enough income coming in to meet your monthly needs. This can be done by holding investments that pay dividends or it can be achieved by selling off some of your investments. Remember that both dividend income and selling will have some tax implications which will require you to incorporate into your calculations.

It is important that we advocate strongly towards investing for the long term and against day trading. If you are very inclined towards day-trading, we advocate that you take a small percentage of your incidental funds and start practicing on that. Any day trading can be done with your funds that you can throw away. Look at it as if it were a highly risky venture. We are not saying not to do this, but do not have this negatively affect your true investment, which will safely guarantee your future. If you are becoming a successful day trader, then you can look to supplementing your investment with any earnings from this activity. This could be considered as one of your side hustles. This area is highly speculative and as such highly risky, only use funds that you are willing to lose.

You have most likely heard the expression, “Do not put all your eggs in one basket.”. We also advocate this when it comes to investing. It is for that reason that for beginners we advocate to invest in index funds, such as Dow Jones, S&P 500 or NASDAQ (National Association of Securities Dealers Automated Quotations). What we advocate for are both Exchange Traded Fund (ETF) and Index funds for now in one of the three markets. There are others and we will cover these issues with diversification.

One area to think about when investing are the fees, this is critical. What are the fees associated with a purchase, is that fee acceptable. If you have a $5 fee on a $1,000 investment, this would be fine, anything less than 1% is decent but aim towards getting this at zero or close to zero, 0.1% is very acceptable. If you are gearing towards an index fund, this is similar to a mutual fund, but it has much fewer fees than an actively traded fund.

How to Invest – Actively Traded Fund versus Passively Traded Fund

Both of these are mutual funds, there is a significant distinction between the two, the actively traded funds have fund managers that actively make trades with the hope of beating the market. The problem is that these trades incur costs and those costs are passed on to the consumer. As well, it is very rare for a fund manager to beat the market, hence, despite being well paid and incurring more fees they still are outperformed by the market. Conversely, a passively traded fund follows set rules and does not make many trades during the year. This fund is set to match the market, hence, its fees are lower and those savings are passed to the consumer. As well, they meet the market, hence, they generally outperform the actively traded funds. Does that mean that you should avoid actively traded mutual funds? For beginners in investing our recommendation would be to avoid those funds and stick to lower costs, less risk and more likelihood to meet market gains as opposed to those that are likely to be outperformed by the market.

Get more information from us – sign up here:

Index Fund vs ETF

How should one decide between an index fund and an ETF? An index fund is a mutual fund with a very low costs ratio, in other words you will not be charged much for annual costs, this could be as low as 0.1%, which is an acceptable level, an actively traded one can have costs as high as 1% or ten times as much, these should be avoided for now. The ETF has even fewer fees and is similar to buying a stock of each of the stocks within the market. Their fees can be as low as 0.05% per year, which is extremely reasonable and acceptable. One also needs to include the cost of purchasing an ETF versus the cost of purchasing an index fund. The index fund may have lower costs in this regard and one would need to combine the two to see which is better. In the long run, having a lower annual cost will pay huge dividends down the road. If we are assuming an 8% return for the index fund, then the ETF may have a return of 8.5%, this will have a great difference down the road. The future value of $1,000 at 8% in 20 years will have a value of $4,661, while the same investment for the same time at 8.5% will have a value of $5,112, which is almost 10% more. Hence, we are strongly advocating to use ETF with the lowest expense ratio.

For more advanced investors we will go into much further detail in another book and speak more about the differences on our website. Our recommendations are geared towards both the beginner investor and the typical investor. There are reasons to use actively traded funds, but you have to understand fully the pros and cons. As well, many day-traders are making a healthy living, however, you must be very well versed in trading to do so. Our recommendations are not for those readers.

For this book, we will focus on some well known Exchange Traded Funds (ETF), while we also recommend Index Funds, our focus is on ETF’s due to their lower expense ratios over time.

We will look at the following: S&P 500, Dow Jones and NASDAQ, as well, we will add in Berkshire Hathaway (BRK-A), while not an ETF, it does carry a portfolio of stocks and hence it is also less risky, since it follows the rule of not putting all of your eggs in one basket.

We have gathered data for each of these over time, some going back over 50 years, we have graphed it out for you. Since we are going so far back, we are graphing the data on January 1 each year. You can also do this every month or even every day. You will get a similar graph but more movement during the year, of course.

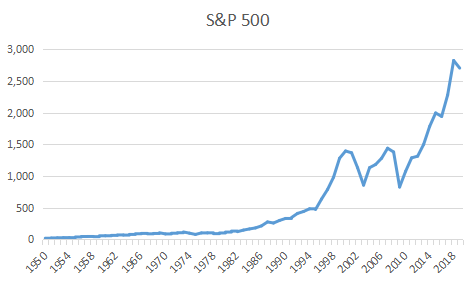

Standard and Poor 500 (S&P 500)

You can see a sharp rise in later years. This is typical of an exponential growth curve, it slopes quickly upward. In the early years, there is slow relative growth and then later it grows more quickly.

Imagine if a stock price doubled every ten years. Let us say the price was $10, in year 0, then ten years later it would be $20, twenty years later it would be at $40, thirty years later it would be at $80 and 50 years later it would be at $160. In the last ten years, it grew by $80, while in the first ten years it only grew by $10. This is the power of investing for a long period and a sure way to build wealth.

Let us look at another market.

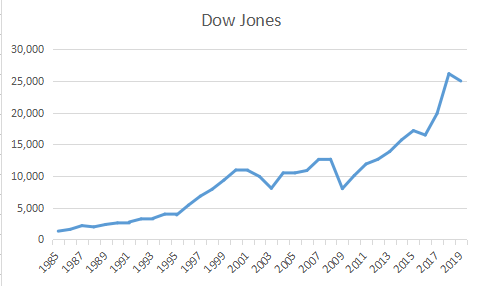

Dow Jones

Similar to the S&P 500, Dow Jones also has an exponential growth curve. This is also a good ETF to hold.

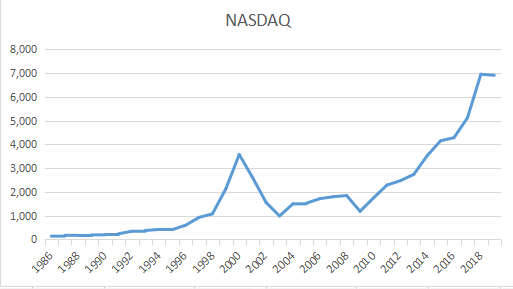

Let us look at NASDAQ, some consider this one a bit riskier, but over the long term, it shows good strength and strong growth.

NASDAQ

Again, we see a strong exponential growth for NASDAQ.

It is important to notice that in all of these markets you can see a great drop in around 1999-2000 and around 2008-2009. Without fail each of them displays this drop.

It is important to understand this, there is a risk with each of these markets and stocks in general, however, if you hold these ETF’s for 20, 30 years or more, you will be very likely to reduce most of your risk and take advantage of strong growth.

You should also invest regularly and overtime. If a market does fall, then keep buying that market for the next years and you will do well over the long run.

If you made a big investment in 1999 and did not invest much further, you still will have earned income but you would have earned more by investing in equal portions in 1999, 2000, 2001 and 2002. The same goes for 2008, you would earn a lot more if you invest as markets rise but also invest as markets fall. You may even earn more by investing more as the markets decrease.

It is important to remember that this strategy is to hold for the long term. This way when the value of an ETF falls, do not consider it as a loss but consider that you are now getting a great deal as you invest more. Use this strategy for ETF’s do not use it for individual stocks. There is a chance that an individual stock goes to zero or goes bankrupt. The likelihood of a whole market being wiped out is far less likely. There was a great market crash in 1929, but those who invested in the 1930s made fortunes.

You are not a day trader with this strategy so do not sell on the losses. Many people panic and sell as a market loses value, this is exactly what you do not want to do. You want to do the opposite, when others are panicking and selling, this is the time to start buying. When others are buying and rising prices of markets, this is the only time one could consider selling. However, do avoid this urge. You are not day trading, you are holding for the long term.

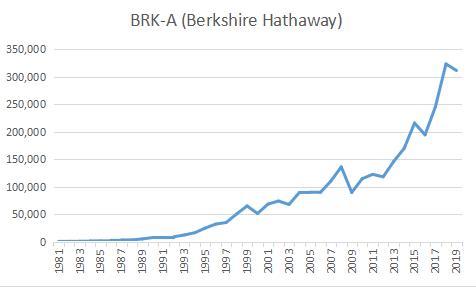

Let us have a look at Warren Buffett’s Berkshire Hathaway stock (BRK-A).

For more information – check out this book on Amazon

BRK-A

Again, we see a strong exponential growth here. Also, we can see that there were some corrections in 1999 and 2008, but there were far less grave corrections. This is and would be a great stock to own. It is the only non-ETF that we recommend holding. The one concern that we do have is that Warren Buffett is now on the older side, while still healthy, he will not live forever. The stock may have a correction when he does pass away. (We do wish him many more years and much health).

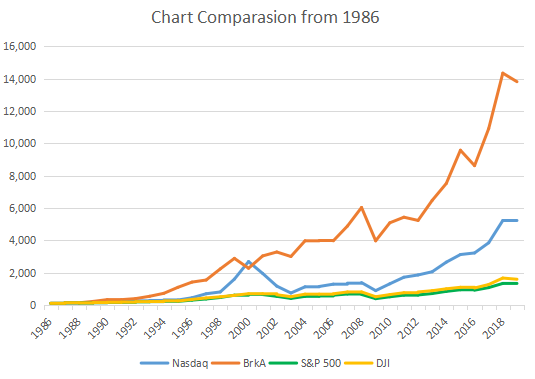

We have now a slide that combines all four of these from 1986 until 2019, to compare, we have set the 1986 value at 100 and put all subsequent values as a ratio of the 1986 price.

Comparison Chart

This chart shows all starting at the same value 100, this way we can see the relative growth to each other. It is clear that BRK-A is the strong winner in this analysis, while NASDAQ also performed quite well, both S&P 500 and Dow Jones were quite similar to Dow Jones having a slight edge on S&P 500.

You can see that there is a great risk with NASDAQ in 2000 – 2003 it lost a lot of value, but over time it recovered and even grew stronger. The growth from 2003 to 2019 was very strong. What is very evident here is the strong growth of BRK-A.

If we look at the 2019 relative values of each, we can see that BRK-A has a relative value of 13,814, this means that it grew a staggering 138 times its starting point since 1986 or in the past 33 years.

If you want to calculate the average annual growth, you can use the Log (base 10 or any base) to calculate that,

To do so, first calculate the growth, it grew from 100 to 13,814, hence it grew 138.14 times (13,814/100) or (end value/start value). Let us take the Log of that which is 2.1403, now divide that number by the number of years, which is 33. This results in 0.64857. The last step is to put that figure back to 10 to the power of, hence, 10^0.64857 yields a value of 1.1610. If we put that in percentage terms after subtracting one (to get growth) we get a value of 16.1% growth over the past 33 years.

To see if our value is correct, use the following formula:

Start value * (1+ growth rate) ^ number of years therefore 100 * 1.161^33 =13,814.

The formula to calculate the average growth is the following:

Growth rate ={10 ^[Log (End value/start Value)]/(number of years)} -1

Following the same formulas, you can see that NASDAQ had a growth rate of 12.7%, while Dow Jones had a rate of 8.7% growth and S&P had a growth rate of 8.0% growth. For this book, we will aim on the side of caution and use a base rate of 8%, but it is clear that this can be higher.

It is important to practice with these formulas and understand how they work. It is also important to see how a little increase in the average growth rate can have a staggering effect in the long run. The average rate in NASDAQ over the past 33 years is 12.7%, while that of the S&P 500 is 8%, both are strong and respectable growth rates, but if you invested $10,000 in each at the start of 1986, by 2019, your value in NASDAQ would now be $519,000 while your value in S&P 500 would only be $121,000. If this $10,000 was invested in BRK-A, with a growth rate of 16.1%, your value would now be $1,381,000.

A good way to start investing would be to focus on these four investment possibilities and focus on holding for the long term. Do not sell, unless there is an urgent need for the funds. Anything that you buy here should be held until retirement. As well, there are tax implications to selling. Most countries will allow you to avoid paying taxes on any gains until you sell the asset. Then you would have to pay a capital gains tax. We do advocate that you are fair and smart with your taxes. Yes, taxes will need to be paid, but best to leave it to when selling your asset, and the longer you hold on to the stocks, the more taxes you can avoid and pay later down the road.

Each country has a different way to calculate taxes, we advise that you consult with a good CPA to see what are your legal options to reduce your tax burden. See our chapter on Taxes for more details.

In summary, we advise going with ETF rather than with individual stocks or mutual funds. The fees attached with mutual funds are very high and those associated with ETF’s are quite low. We advise against day-trading and actually advocate for the opposite approach which is holding for the long term and only selling when required or as part of your revenues during retirement.

When we look at active trading versus passive trading, we advocate fully on passive trading. Most of the hedge funds or fund experts are on the side of active trading. This makes sense, they are putting years of education and experience to practice to beat the market. The reality is that most of these do not beat the market. They may beat the market for one year or even two, but over a long period, they lose to the market. Think about the implication of this. In other words, there are hedge fund managers who are paid excessive sums per year who you can beat by simply choosing to invest in a strong ETF as one of the four options that are mentioned here (BRK-A is not an ETF, but a great option to include). This little understood fact is one that you should always keep in mind. There will be many people advising you to invest in this or that mutual fund. Do resist the urge, put your money in areas where the fees are far less and where the results are far better. The fees are one of the main reasons that those funds perform worse than the market. Imagine the market performs at 8% with little to no fees, now a hedge fund with a fee of 1%, has to now earn 9% just to stay on par. The higher the fees the worse they perform. As well, with active funds there is more chance of sales and buys, also increasing costs and generally under-performing. Stay away from all actively managed funds. If a person could outperform the market, even by 1% or 2%, that person could earn whatever sum they desired.

The only well-known person to be able to achieve these results is Warren Buffett, his net worth is a staggering sum, he is one of the wealthiest people in the world. He follows an approach that is similar and holds for the long term and does not follow day trading. Better to invest in BRK-A or BRK-B than any mutual fund.